China

China  India

India  Japan

Japan  Philippines

Philippines  Singapore

Singapore  South Africa

South Africa  Sri Lanka

Sri Lanka  Thailand

Thailand  Colombia

Colombia  Ecuador

Ecuador  Austria

Austria  Denmark

Denmark  Finland

Finland  France

France  Germany

Germany  Hungary

Hungary  Norway

Norway  Poland

Poland  Portugal

Portugal  Romania

Romania  Spain

Spain  Sweden

Sweden  Switzerland

Switzerland  United Kingdom

United Kingdom  UAE

UAE  Canada

Canada  Mexico

Mexico  United States

United States .svg)

Open banking is the banking practice of sharing consumer financial data between third-party financial service providers (TPPs) and banking and non-banking institutions through APIs. These TPPs are mostly fintechs who benefit from this data to offer a wide range of services like payments, data aggregation, and analysis.

The Open API ecosystem in banking has opened a gateway for innovative customer servicing while boosting business growth and competition within the financial sector. How has it done so? The secret lies in giving service providers access to your financial information in a secure manner.

The concept of open consumer financial data has travelled from Europe and UK to other parts of the world, influencing the growth of financial aggregators and fintechs. In this blog, we will look at how this idea evolved and what kind of future beckons this domain.

What sparked the change?

Self-service banking started way back in the 1980s, evolving continuously from online banking via screen text by Norisbank to banking via PIN/TAN passwords by FinTs (HBCI), from web screen-scraping by Sofortüberweisung to the legal action by Giropay for unfair competition. In 2015, the PSD2 enforced by the European Commission led to the practices of adoption, competition, and innovation through APIs in the banking sector. Such small technological steps taken by traditional banks over the last 40 years eventually paved the way for open banking.

Customer servicing - from a bold, new perspective

Who could have thought the idea of open banking APIs would have the potential to revolutionize targeted customer servicing? Open banking has grown from the original idea of payment information services (PIS) to account information services (AIS).

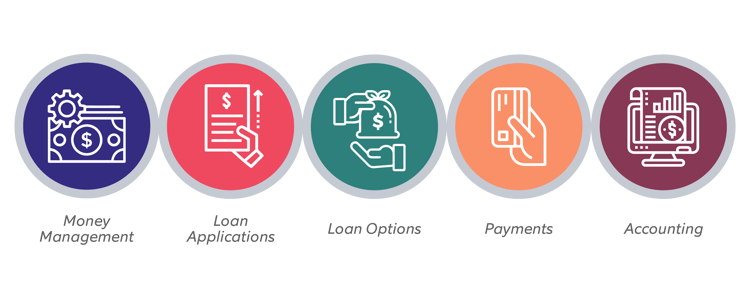

- Money management - A 360° real-time view of a customer’s assets, liabilities, and transactions, allows them to analyze and manage their expenses, budgets, and investments in a much better way. The Connected Money app from HSBC is one such app that allows customers to view all their accounts in one place.

- Loan applications - With platforms enabling customers to access their bank accounts and pull out transactional data for credit analysis, it has become easier for customers (especially those with ‘thin’ profiles) to get credit approvals.

- Loan options - This is a comparison platform for loan offers that uses a customer’s personal and financial data to display different offers to choose from. Bank Bazaar and Policy Bazaar are such online platforms that compare offers from different banks for financial instruments in return for customer data.

- Payments - Several e-wallet services like Paytm and PayPal reward (and encourage) their customers for making high-value or frequent transactions. On the other hand, merchants benefit substantially by avoiding chargebacks on rejected or fraudulent payments due to direct transactions between the consumer and the bank. A direct transaction like a money transfer also guarantees instant payment to the merchant, thus providing cash liquidity.

- Accounting - Companies like Nordic API Gateway offer both AIS and PIS to empower the accounting industry and allow significant time for funds to appear.

A big win for the fintechs

With the Competition and Markets Authority in the UK and PSD2 in Europe, fintechs are expanding into multiple financial services and are giving tough competition to the banks. Yapily, a fintech that is already a leading name in the open banking world, partnered with American Express as the multi-national financial services giant saw an opportunity to leverage the Yapily’s open APIs for its payment services.

However, in geographies other than Europe and the UK where open banking is market-driven, small fintechs and financial institutions struggle for customer data to provide services to compete with banks. Open banking APIs help in capturing and retaining this data. Fintechs also see opportunities through money management services that require customer account aggregation. This provides insights to the owning fintech about the customer’s portfolio.

Open banking is one of the latest trends in digital lending. After COVID-19, banks and fintechs have evolved their credit underwriting process using open banking APIs to get customer financial data. This reduces a great deal of financial fraud risk and expedites the loan underwriting process.

According to the World Fintech Report from Capgemini, 89% of the banks leverage APIs to collaborate with fintech firms as part of their business strategy.

The concept has also enabled several businesses to expand from their core businesses to financial services. Chinese multinational technology company Alibaba that specializes in retail business and e-commerce expanded into a third-party online payments platform Alipay (now Ant Financial Services). Singaporean MNC Grab providing taxi-booking services to customers, expanded into GrabPay, and acquired Indonesian Ovo to build API-drive payment services.

Investors are continuing to deploy capital to European fintech players, participating in 90 deals, totalling $1.67 billion in q3’19.

What can the banks get from all this?

While the banks are not at the perfect receiving end of the open banking strategy, some banks are now using this tool themselves to compete with the fintechs.

Banking-as-a-Service: To compete with the digitalization of fintechs, banks with legacy systems are now using plug-and-play services on their websites. An example of such a service can be a credit score check service that uses the customer’s financial data with the bank in exchange for a real-time credit score by credit bureaus. Experian Connect API and Equifax’s API Connect are two such open banking APIs. Some banks are also developing their open banking solutions like HSBC’s Connected Money app, competing at the same level as a TPP. Banks can also collaborate with financial aggregators and open banking platforms to offer customer services to challenge fintechs. An example of this is the Nordic challenger bank Lunar, which has recently tied up with Nordic API Gateway, an open API platform, to create a ‘financial super app’. Banks can utilize the open API solutions to strengthen relations with their existing customers, which they built through years of customer engagement.

Building API layers helps banks move from core banking to core-less banking, thus accelerating continuous delivery and improving operational efficiency.

What do we see in the future?

With the current developments, we can assume open banking is here to stay. For the “underserved” customer segment, banks will come up with flexible financial services to expand their geographical footprint, where established fintechs already have a presence. Fintechs, on the other hand, will need to come up with more innovative solutions once banks, backed by their strong brand value, decide to move into an open API strategy. While both compete for better customer services, the customers will be the ultimate beneficiaries, which accomplishes the objective of financial inclusion for all customers.

If you are a financial services institution looking to offer innovative solutions and better customer service, we can help you! Explore our offerings and connect with our experts today!