China

China  India

India  Japan

Japan  Philippines

Philippines  Singapore

Singapore  South Africa

South Africa  Sri Lanka

Sri Lanka  Thailand

Thailand  Colombia

Colombia  Ecuador

Ecuador  Austria

Austria  Denmark

Denmark  Finland

Finland  France

France  Germany

Germany  Hungary

Hungary  Norway

Norway  Poland

Poland  Portugal

Portugal  Romania

Romania  Spain

Spain  Sweden

Sweden  Switzerland

Switzerland  United Kingdom

United Kingdom  UAE

UAE  Canada

Canada  Mexico

Mexico  United States

United States .svg)

Ever changing regulations in the BFSI world are obliging banks, financial institutions, and insurance companies to find ways to better protect their customers. On top of that, in an era of hyper-personalization, customers have come to expect an experience that revolves around their needs. How can businesses bridge the gap between their generic offerings and the more personalized service customers demand today?

Know Your Customer (KYC) is the first step in a customer’s relationship with any business. While it is crucial for all sectors, it is especially relevant in banking and financial areas and related sectors such as insurance, trading, etc.

In this blog, we will explain the KYC process, the challenges around traditional models, and the different ways through which banks and financial institutions can leverage technology to create an effective KYC solution.

The KYC process and its components

Right from customer onboarding, all banks and Financial Institutions (FIs) must perform the KYC process regularly to:

- identify their customers,

- verify and reconfirm the information, and

- assess the customer’s risk.

An effective KYC process in banks and financial institutions should have the following three components:

1. Customer Identification Process:

The Customer Identification Process (CIP) begins during onboarding. The financial institutions capture basic customer information (like full name, date of birth, address, identification number) to authenticate the customer. For a business, FIs can request extra information such as a business address, ownership details, business identification number (like Tax Identification Number), etc. The collected information may vary based on the type of account/product, compliance policy, geography, and associated regulations.

2. Customer Due Diligence:

Customer Due Diligence (CDD) involves conducting a detailed assessment of the new client from an Anti-money Laundering (AML) perspective. The output of CDD is generally a risk rating, i.e., low, medium, or high-risk. Some high-risk customers are even passed through Enhanced Due Diligence (EDD), which provides greater scrutiny.

3. Continuous Monitoring and Reporting:

This step involves monitoring the account and transactions to track suspicious activities and reporting them to the appropriate authority. Continuous monitoring is an essential part of effective KYC and anti-money laundering procedures. Banks/financial institutions should perform ongoing due diligence for every customer. This helps examine the transactions closely to ensure that they are consistent with the customer’s profile and source of funds as per extant instructions.

Any bank or financial institution needs to have a proper KYC framework as per the local regulations. Any non-compliance can result in penalties being imposed on the banks.

In 2019 alone, global penalties worth $36 billion were imposed for non-compliance with AML, KYC, and sanctions regulations.

Challenges in traditional KYC models

Traditional solutions depend on manual processes and comprise challenges, such as:

- Inefficient operations due to high data volume, customers having multiple identities within a bank, etc.

- Bad customer experience due to slow process, delayed onboarding, or one-size-fits-all solutions.

- Ineffective compliance checks to fight fraud due to data quality issues, slow updates of dynamic risk profiles, lack of consolidated view of customer data, inability to respond to frequent changes in regulations, etc.

Financial institutions need technological solutions to help navigate the regulations. This is why there is a sharp increase in the number of start-ups around regulatory technology or “regtechs”, with around $ 9.5 billion invested (from 2014-18) in them. Almost 60% of these start-ups are focused specifically on solving KYC/AML issues.

Effective KYC/AML solution

Any robust KYC/AML and due diligence solution for the customer must include:

- Digital mechanisms to capture customer information, leverage multiple third-party and government databases to validate the information, and improve data quality.

- Ability to verify identity documents using technologies like Biometrics, ID Verification, RPA, OCR, etc.

- Data visualization for 360-degree customer view for various internal teams (like security, operations, forensics, AML, etc.) to get complete customer details and understand the associated risks. This can even be coupled with dedupe checks through name-matching algorithms, using AI/ML/NLP-based solutions.

- Regular knowledge about existing customers, providing financial institutions with the right customer insights and an opportunity to offer a personalized customer experience.

- Customer screening through various screening lists such as Politically Exposed Person (PEP) list, sanctions list, Office of Foreign Assets Control (OFAC), or other third-party or government data.

- Risk profiling the customers to segment them. Low-risk customers can have seamless onboarding, and high-risk customers can be screened for further due diligence.

- Process automation in selective processes. For example, an automated approval mechanism for low-risk customers.

- With an increase of digital data availability, the KYC solutions must adapt and account for these new data points to ensure better customer assessment.

- AI/ML algorithms process huge amounts of unstructured customer or business data, including data related to adverse news/events, social media, affiliates, businesses, third parties, and transactions.

- Continued due diligence for the entire lifecycle of the customer account so that any transactions that are not per the customer’s risk profile or are suspicious w.r.t the amount, source of funds, beneficiary names, etc., can be tracked and reported.

- While we should aim to have a completely digital process, there could still be scope for some manual intervention. Low code tools can be used to orchestrate the workflow in this case.

- Controls around data privacy and cybersecurity so that customer information can remain confidential.

- With the growth in the types of mobile devices, the solution should work across different channels.

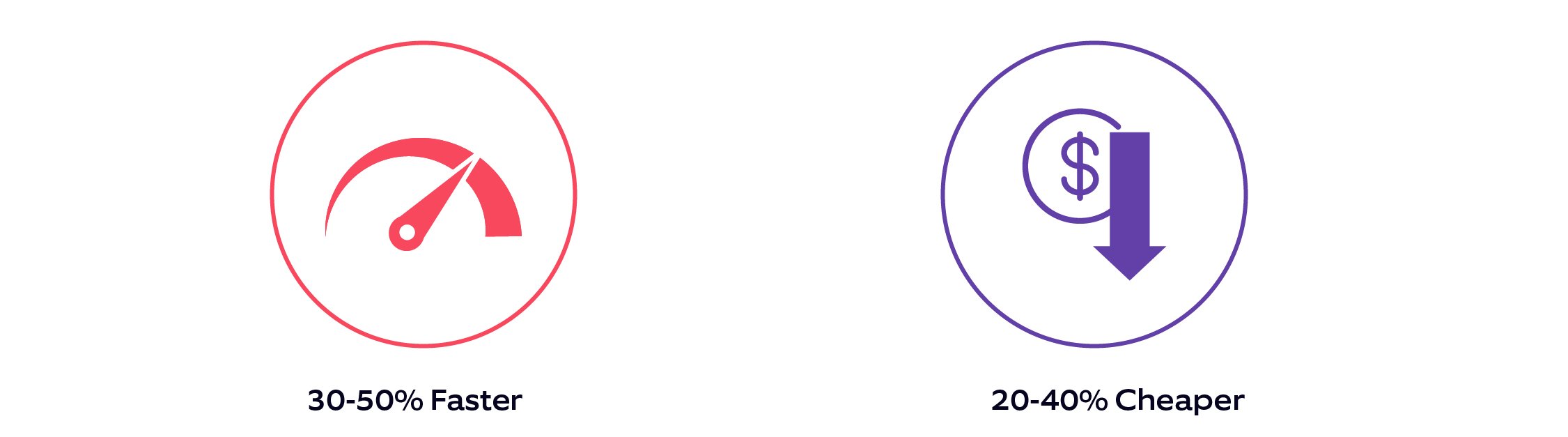

According to PwC, a streamlined KYC process can provide a standardized and efficient service that can be up to:

Final thoughts

KYC is one of the most important processes in the financial industry as it impacts the customer, regulator, financial institution, and even the government. Moreover, globalization has led to a spike in the volume of cross-border transactions, making financial institutions more exposed to money laundering activities. This makes it even more challenging for them to operate in multiple nations to comply with country-specific regulations.

Every financial institution aspires to build brands. But no brand would like to be associated with individuals or businesses with a bad name. There is a big reputational risk involved in such associations. On the other hand, if set up correctly, the KYC/AML process could also benefit the customers by providing a personalized experience.

With technology as an aid, the rules of the game are changing and the financial institutions that embrace innovative KYC solutions can gain a competitive edge.

Do you want to leverage technology to build an effective KYC/AML solution? Our experts are here to help. Check out our offerings and get in touch with us!